Automotive Blog

How to Claim Car Insurance After an Accident in India

A car accident is something every driver hopes to avoid, but unfortunately, it can happen to anyone. Whether it's a minor bumper scrape in city traffic or a serious collision on a highway, accidents often occur without warning. In those stressful moments, most people focus on the safety of passengers and the condition of their vehicle. However, once the immediate situation is under control, another important question arises: How do you claim car insurance after an accident?

For many vehicle owners in India, especially first-time car buyers, the car insurance claim process can seem confusing. Terms like cashless claim, surveyor inspection, Own Damage claim, and No Claim Bonus may sound complicated if you've never dealt with them before. As a result, many people make mistakes that delay their claim or reduce the amount they receive from the insurer. Many of these errors are similar to the common car insurance mistakes that buyers make even before taking delivery of a new vehicle.

The good news is that claiming car insurance in India is not as difficult as it may appear. Insurance companies have streamlined the process over the years, and many now allow policyholders to register claims online, upload documents digitally, and track claim status through mobile applications.

In this guide, we'll walk you through everything you need to know about the car insurance claim process in India. Whether you've recently been involved in an accident or simply want to understand the procedure before you ever need it, this article will help you navigate the process confidently and avoid common mistakes.

Why Understanding the Car Insurance Claim Process Is Important

Most people purchase car insurance because it is mandatory by law or because they want financial protection against unexpected expenses. However, very few vehicle owners spend time understanding how the claim process actually works.

Imagine this situation. You have a comprehensive car insurance policy and are involved in a minor accident. The damage to your vehicle is significant enough to require repairs costing ₹40,000. Since you have insurance, you expect the company to cover the expenses. But if you fail to inform the insurer on time or begin repairs before the vehicle is inspected, your claim could face delays or complications.

Understanding the correct procedure beforehand can save time, reduce stress, and increase the chances of a smooth claim settlement. It also helps you make informed decisions about whether to file a claim, how to protect your No Claim Bonus (NCB), and which repair option is most suitable for your situation.

What Should You Do Immediately After a Car Accident?

The moments following an accident are critical. While it's natural to feel nervous or frustrated, staying calm and taking the right steps can make a significant difference to both your safety and your insurance claim.

The first priority should always be the well-being of everyone involved. Check yourself, your passengers, and anyone else involved in the accident for injuries. If medical attention is needed, contact emergency services immediately. Even if injuries appear minor, it is often wise to seek medical evaluation, especially in the case of high-impact accidents.

Once safety concerns have been addressed, assess the condition of the vehicles. If the accident is minor and the vehicle can be moved safely, relocate it to the side of the road to avoid obstructing traffic. However, if the accident is serious, it may be better to leave the vehicle in place until authorities arrive.

One mistake many drivers make is failing to document the accident scene properly. Your smartphone can become one of your most valuable tools during this process. Take photographs from multiple angles, showing the damage to all vehicles involved. Capture road conditions, traffic signs, skid marks, and any other details that may help explain how the accident occurred.

If another driver is involved, exchange information politely and professionally. Collect their name, contact details, vehicle registration number, and insurance information if available. Avoid arguments or admissions of fault at the scene, as the insurance company and authorities will determine liability based on evidence.

Most importantly, notify your insurance company as soon as possible. Many insurers offer 24/7 claim support and encourage policyholders to report accidents immediately. Delayed reporting can sometimes complicate the claim process and may even affect claim approval in certain situations.

Understanding Different Types of Car Insurance Claims

Before filing a claim, it's important to understand which type of claim applies to your situation. Different accidents lead to different claim processes, and knowing the difference can help you communicate effectively with your insurer.

The most common type is an Own Damage Claim. As the name suggests, this claim covers damage to your own vehicle resulting from an accident, natural disaster, fire, theft, or similar incidents. If your car hits a divider, collides with another vehicle, or suffers damage during a flood, you would typically file an Own Damage claim.

Another category is the Third-Party Claim. This applies when your vehicle causes injury, death, or property damage to another person. Third-party insurance is mandatory in India because it protects individuals who suffer losses due to accidents caused by other drivers.

Most private vehicle owners today opt for Comprehensive Car Insurance, which combines Own Damage coverage with Third-Party Liability coverage. If you're unsure whether a standard comprehensive policy is enough, it's worth understanding the differences between Zero Depreciation and Comprehensive Car Insurance before choosing coverage. Comprehensive policies provide broader protection and are generally recommended for cars of all ages.

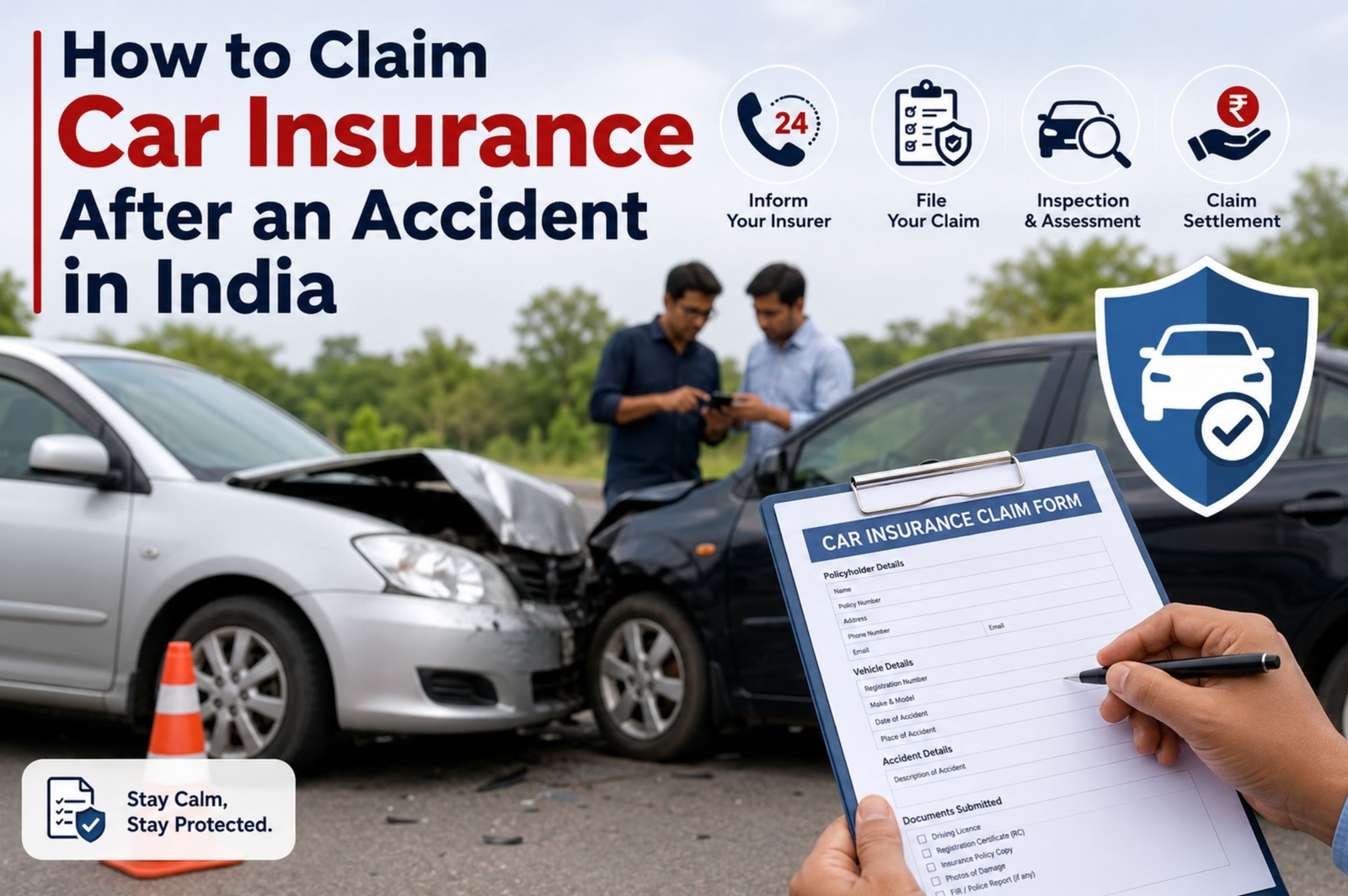

How the Car Insurance Claim Process Works in India

Once the accident has been reported, the claim process officially begins. Although procedures may vary slightly between insurance companies, the overall process remains largely the same.

After receiving your accident report, the insurer registers the claim and assigns a claim reference number. This number allows both you and the insurer to track the status of the claim throughout the process.

The next step usually involves a vehicle inspection. The insurance company may appoint a surveyor to assess the extent of the damage. The surveyor's role is to verify the claim, inspect the vehicle, estimate repair costs, and submit a report to the insurer.

This inspection is extremely important because it forms the basis of the claim settlement amount. For this reason, you should generally avoid undertaking major repairs before the surveyor completes the assessment unless the insurer specifically authorizes it.

After inspection, you'll be required to submit supporting documents. These commonly include your insurance policy details, vehicle registration certificate, driving licence, claim form, repair estimate, and photographs of the damage. Depending on the circumstances, additional documents such as an FIR or police report may also be required.

Once documentation is verified and repairs are approved, the insurer proceeds with claim settlement based on the policy terms and the surveyor's findings.

Cashless Claims vs Reimbursement Claims: Which One Is Better?

One of the most important decisions during the claim process involves choosing between a cashless claim and a reimbursement claim.

A cashless claim is generally considered the most convenient option. Under this arrangement, the vehicle is repaired at a network garage approved by the insurer. The insurance company directly settles the eligible repair costs with the garage, reducing your out-of-pocket expenses.

For example, suppose your repair bill amounts to ₹60,000 and the approved claim amount is ₹52,000. In a cashless claim, the insurer pays the approved amount directly to the garage, while you pay any remaining charges, deductibles, or non-covered expenses.

A reimbursement claim works differently. In this case, you pay the repair costs yourself and later submit bills and supporting documents to the insurer. After verification, the insurer reimburses the approved amount.

While reimbursement claims offer flexibility in choosing any repair workshop, they usually involve more paperwork and longer processing times.

For most car owners, cashless claims provide a smoother and faster experience.

Is an FIR Required for a Car Insurance Claim?

This is one of the most frequently asked questions among policyholders.

The answer depends on the nature of the accident. For minor accidents involving only your own vehicle, many insurers may process claims without requiring an FIR. However, there are situations where filing an FIR becomes important or mandatory.

For example, an FIR is generally required in cases involving vehicle theft, serious injuries, death, third-party liabilities, major property damage, or hit-and-run incidents. Police documentation helps establish the facts of the case and supports the claim investigation.

Even when an FIR is not mandatory, it is always advisable to follow your insurer's guidance and local legal requirements.

Common Reasons Why Car Insurance Claims Get Rejected

Many policyholders assume that having an insurance policy guarantees claim approval. Unfortunately, that isn't always true.

Insurance companies can reject claims if policy terms are violated or if required procedures are not followed.

One common reason is delayed reporting. If the insurer learns about the accident several days later, it may become difficult to verify the circumstances. Another common issue is driving without a valid licence. Insurance policies generally require the driver to possess a valid driving licence at the time of the accident.

Claims may also be rejected if the driver was under the influence of alcohol or drugs, if the policy had expired, or if false information was provided during claim registration.

Unauthorized repairs before vehicle inspection can also create complications because the insurer loses the opportunity to independently assess the damage.

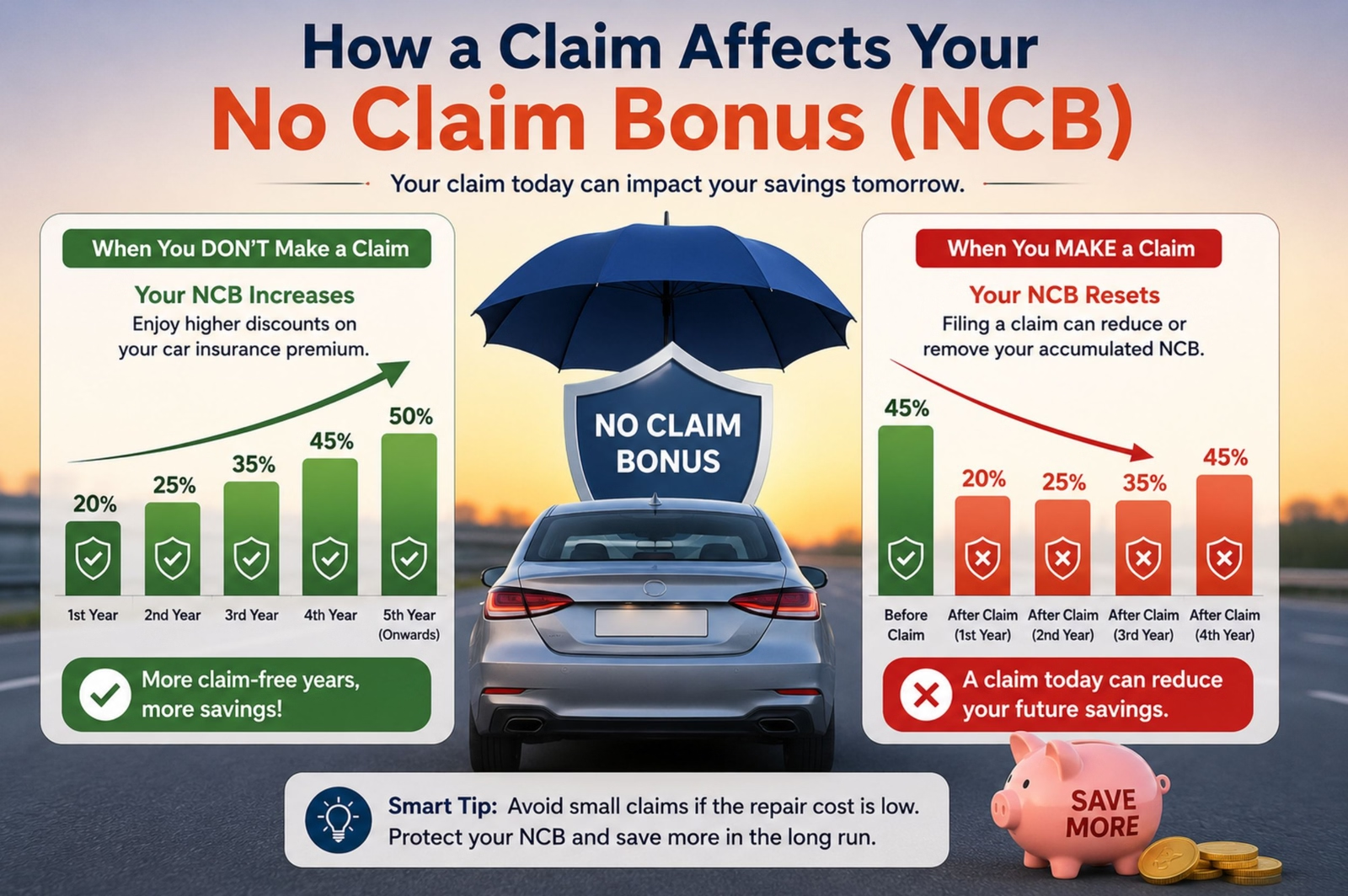

How a Claim Affects Your No Claim Bonus (NCB)

Many drivers are surprised when they discover that filing a claim can impact their No Claim Bonus.

NCB is a reward offered by insurance companies to policyholders who complete a policy year without making a claim. Over time, these discounts can become significant and reduce renewal premiums considerably.

When you file an Own Damage claim, your NCB may be reduced or reset during the next renewal. This is why some vehicle owners choose not to file claims for minor damages and instead pay for small repairs themselves.

However, some insurers offer an NCB Protection Add-on that helps preserve the bonus even after certain claims. If maintaining your NCB is important, reviewing add-on options during policy purchase may be worthwhile.

Practical Tips to Ensure Faster Claim Approval

While every claim is different, certain practices can significantly improve the chances of a smooth settlement.

Prompt accident reporting remains one of the most important factors. Early reporting helps establish credibility and allows insurers to begin the investigation quickly.

Maintaining organized records is equally important. Keep digital copies of your policy documents, driving licence, RC, and previous claim records. Having these documents readily available can save valuable time during emergencies.

Using an insurer-approved network garage whenever possible can also streamline the process. These garages are familiar with claim procedures and often coordinate directly with insurers.

Finally, take time to understand your policy before an accident occurs. Knowing your coverage limits, deductibles, exclusions, and add-ons can prevent unpleasant surprises during claim settlement.

Final Thoughts

A car accident can be an unpleasant experience, but understanding the insurance claim process can make the aftermath far less stressful. The key is to stay calm, prioritize safety, document everything carefully, and notify your insurer without delay.

Car insurance exists to protect you from unexpected financial burdens, but successful claim settlement depends on following the correct procedure. Whether you're dealing with a minor accident or a major collision, being prepared and informed can help you navigate the process confidently.

By understanding how to claim car insurance after an accident in India, you'll not only improve your chances of a hassle-free settlement but also gain greater confidence as a responsible vehicle owner. A few minutes spent learning the process today could save you considerable time, money, and frustration in the future.

Written by Team CarBike4U

Editorial & Research Team

CarBike4U's dedicated editorial team researches, reviews, and updates content to bring you the most accurate automotive news, pricing, comparisons, and ownership guidance.